A pay yourself first budget automatically moves money to savings or investments before you pay bills and spend. It’s a powerful system, but it isn’t perfect for every season of life.

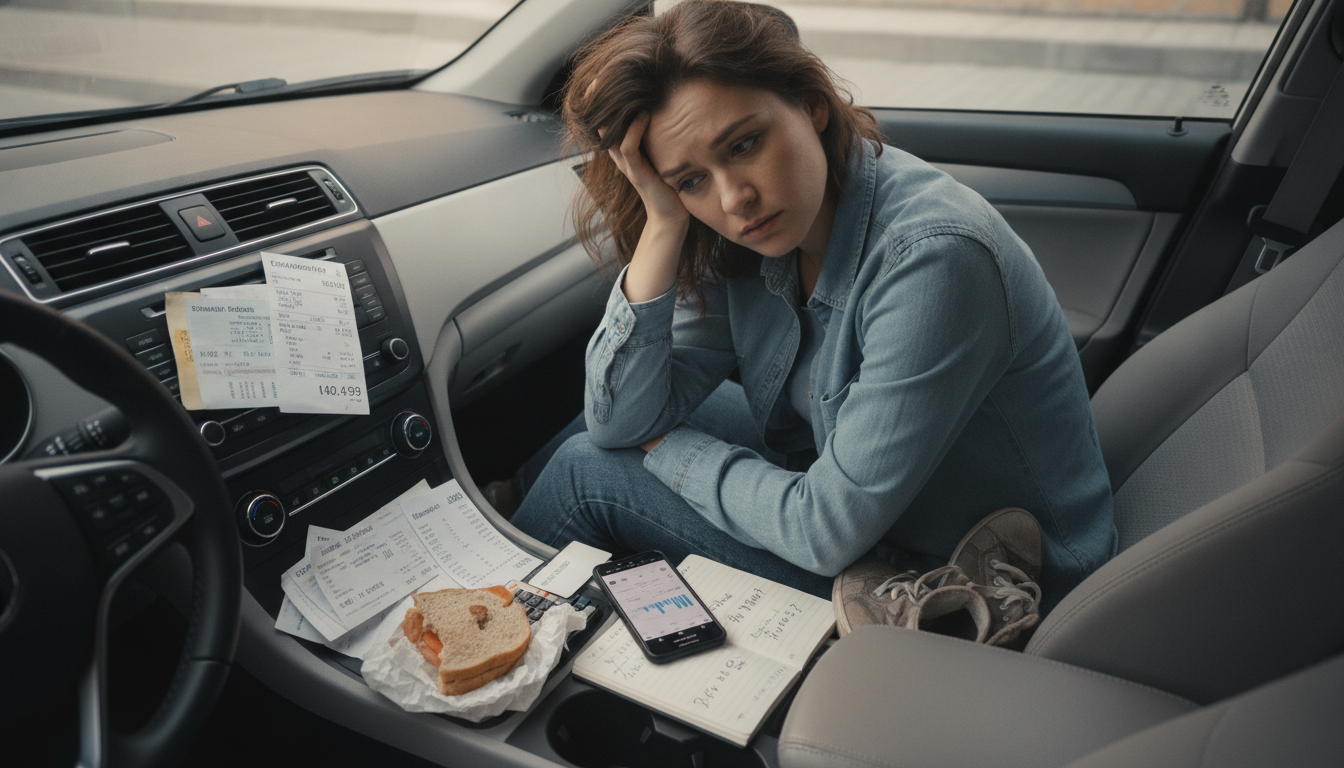

If your transfer happens before key bills clear, you may end up juggling due dates, triggering overdraft fees, or relying on credit cards. This is especially common when paychecks arrive on irregular dates or when multiple bills hit early in the month.

When the savings percentage is too aggressive, necessities like groceries, transportation, prescriptions, or childcare can get squeezed. The method works best when “fixed must-pays” are mapped out first so saving doesn’t compete with keeping the lights on.

Freelancers, commission-based workers, and small business owners can struggle with a set automatic transfer. In low-income months, the same transfer amount can force late payments; in high-income months, you might miss the opportunity to save more unless you actively adjust.

Because saving happens automatically, it’s easy to ignore the spending side. If discretionary purchases remain unchecked, the “leftover” account can run dry, leading to debt that offsets your savings progress.

Transfers timed incorrectly or routed to the wrong account can cause fees, missed bill payments, or unnecessary account shuffling. Periodic check-ins are still required, even with a set-it-and-forget-it approach.

Putting money into long-term savings while carrying high-interest debt or lacking a starter emergency fund can backfire. The method needs an order of operations that fits your current risk level and financial obligations.

If you want a practical way to set it up while avoiding common missteps, see the full guide here: pay yourself first—how to automate savings and build wealth.

Start with an amount that won’t jeopardize rent/mortgage, utilities, food, and minimum debt payments, then increase it gradually as your cash flow stabilizes. Many people begin with 5% to 10% and adjust after one or two full billing cycles.

Leave a comment